Unlocking the Power of Bank Deposit Data: Evidence from Professor Francesco Mazzola’s Research on Open Banking

Traditionally, banks have held a monopoly on customer financial data, using insights from transactions and payment behaviour to assess borrower risk more effectively than new entrants in the financial sector. This exclusive access has led to market concentration, raising concerns about efficiency and financial inclusion (World Bank Group).

The rise of digital finance, combined with advances in data-sharing technology such as secure APIs (Application Programming Interfaces), has prompted governments worldwide to rethink who should control financial data. Open Banking (OB) is at the heart of this transformation, allowing consumers to give third-party financial service providers—such as fintech firms and competing banks—access to their account information and transaction history.

In a recently published article in the Journal of Financial Economics, ESCP Assistant Professor of Finance, Dr Francesco Mazzola and his co-authors examine the key drivers and disruptive effects of Open Banking on financial markets, competition, and innovation.

The Open Banking policies dataset

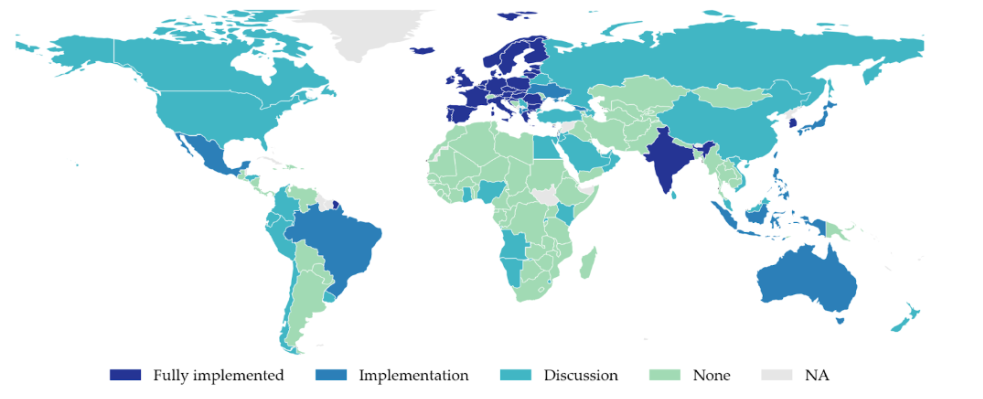

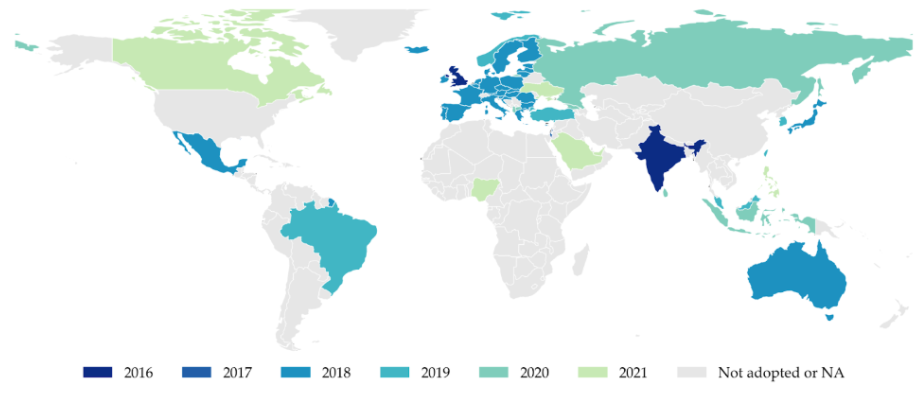

Professor Mazzola and his team have compiled the first comprehensive global dataset on Open Banking policies, mapping out government-led initiatives across 49 countries that have adopted OB regulations, with another 80 countries actively discussing their implementation. Notably, the European Union introduced a unified Open Banking framework under the Revised Payment Services Directive (PSD2, EU Directive 2015/236), requiring all member states to integrate its provisions into their national banking regulations.

Their findings reveal a key insight: consumer trust in data sharing—rather than standard economic or financial factors—plays a crucial role in a country’s decision to implement Open Banking. When consumers are more comfortable sharing their financial data with fintech firms, OB adoption becomes significantly more likely.

Consumer willingness to share their data increases the potential benefits of Open Banking policies.

Francesco Mazzola

Francesco MazzolaProfessor at ESCP Business School

Figure 1: Government-led Open Banking regimes around the world. This map shows the implementation status of Open Banking policies as of October 2021, along with the passage years of key regulations. Panel (a) highlights implementation progress, while Panel (b) indicates when key policies were passed

(a) Government open banking policy implementation status

(b) Timeline of Open Banking adoption

How Open Banking Drives Innovation and Competition

A fundamental policy question is whether Open Banking fosters innovation, competition, and financial transparency, while offering tangible benefits to both consumers and businesses.

Professor Mazzola’s research provides compelling evidence that Open Banking boosts venture capital (VC) investment in fintech firms, driving the development of new financial services, including:

- Budgeting and personal finance apps

- Payment platforms

- Regulatory technology (RegTech)

- Lending and credit services

By analysing micro-level data from the UK, one of the first adopters of Open Banking, the study identifies significant shifts in financial markets:

1. Consumer Finance

- Consumers who share their financial data are more likely to access better financial advice and credit products.

- Open Banking improves financial literacy and increases credit access, particularly for individuals who have missed bill payments.

2. SME Lending & Credit Access

- Examining the UK’s "Commercial Credit Data Sharing" (CCDS) policy—an Open Banking initiative for small and medium-sized enterprises (SMEs)—reveals a 25% increase in non-bank lending relationships.

- Small businesses benefit from lower borrowing costs and greater access to alternative credit providers.

Balancing Innovation and Financial Inclusion

While Open Banking enhances competition, the research also highlights potential downsides:

- Consumers who opt out of data sharing may inadvertently signal that they are higher risk, leading to increased borrowing costs.

- This creates a financial inclusion paradox, where the most privacy-conscious consumers—often already on the margins of the financial system—face unintended disadvantages.

While Open Banking unambiguously increases competition, it can sometimes come at the cost of financial inclusion.

Francesco MazzolaProfessor at ESCP Business School

Conclusion: The Future of Open Banking

The study underscores both the opportunities and challenges presented by Open Banking. While it drives competition and financial innovation, its impact on privacy, risk assessment, and financial inclusion requires careful regulation and oversight.

Professor Mazzola’s research provides a critical foundation for financial regulators, banks, and fintech firms as they navigate this new era of data-driven finance.

Read the full article to explore the implications of Open Banking for the financial services industry.

Professor Francesco Mazzola discusses his research on Open Banking

Campuses